(See other

Monthly Status Updates)

So after five months I've had a great run, followed by an avalanche of Late notes. I think I've had a total of 13 notes that have gone Late. One of them I've been able to sell off.

Every one of the Notes that have gone Late have made payments, but none of them have made payments to me. They were never late and were current when I bought the Notes (assuming that is what those checkboxes mean when Browsing Notes).

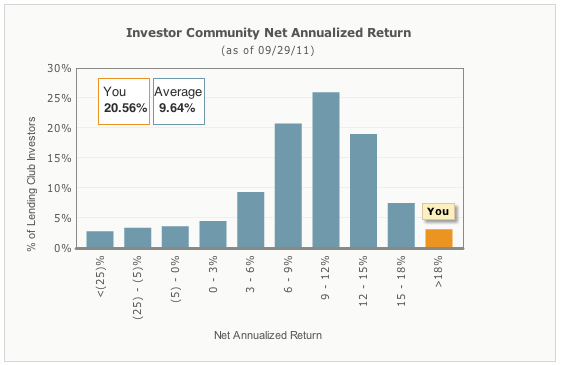

When they give my return, they obviously don't take into account that the Late notes are as good as gone. The chart above shows that of the Notes that go past 31 days, you have basically a 50/50 chance of getting any money back (they don't specify how many were fully recovered versus partially recovered, and how much that partially is). The site reports my return as over 21%. They no longer show your percentile. When they did show it, I had dropped solidly into the 99% (before I was waffling between being in the top 99% and 100%). My own internal reporting needs to change. I've been calculating my account value as the sum of what I paid for all my notes. What I need to use is the lesser of what I paid or what I am asking. I believe that will more closely represent my account value.

Of course, it may be more representative to consider Late Notes to be $0. I don't know what the conversion rate from Grace Period to Late is, but from 16-30 Days Late to 30-120 Days Late has been 100% for me. I've been able to stem the tide of Late Notes by being more aggressive at selling Grace Period Notes. I've still had a few slip into Late status.

I've been selling Grace Period Notes at 80% of P+I (rounded down to the nearest dollar), and dropping the price by $0.10/day. Some of these Grace Period Notes have received payment and then sold at this discount. At first I was disappointed, but then I realized I didn't want the notes where the borrower was willing to go into Grace Period.

Late 16-30 Days I sell at 75% of P+I (rounded down to the nearest dollar), and dropping the price by $0.10/day. Late 31-120 Days I sell at 50% of P+I (rounded down to the nearest dollar), and dropping the price by $0.10/day. Not that discounting Late Notes seems to work. I have only sold one Late Note, and none have returned from the grave. I may consider being more aggressive at selling Grace Period Notes just to prevent Lates, since they seem to be the land of no return.

Most of my Notes (almost 2/3) are still F Grade. If I read the numbers correctly, 76% of the F Grade Notes are still Active (Current or Late). Of the Active F Grade Notes, 95% of them are Current. 25% of my Late Notes are F Grade while the compose 63% of all my notes. It appears that F Grade Notes are a pretty sweat spot.

E Grade Notes have roughly the same Current, Late and Default rates. They are also about 25% of my Late Notes. However, they only comprise 6% of my portfolio. So apparently I've been really unlucky with E Grade Notes.

Half of my Late Notes are G Grade. Given that about 1/3 of my portfolio is G Grade and that the stats for G Grade notes is a bit worse (91% of Active Notes are Current as opposed to 95% for E and F) that is not surprising. About 8-9% of E and F Grade Notes are in Default. For G Grade Notes, it's 14%.

You would think that due to the very small place that E Grade Notes hold in my portfolio (and that they are statistically equivalent to F Grade Notes) that they would not hold such a prominent spot in my Late Notes.

It is also interesting to see what Lending Club is doing to attempt to reclaim my money from the Late Notes. Below is a chart of the latest action Lending Club has taken on the Late Notes.

| Months Old | Payments Made | Latest Action |

|---|

| 3 | 2 | Sent email to borrower |

| 4 | 7 | PAYMENT Failed |

| 5 | 2 | Borrower contacted Lending Club |

| 5 | 3 | Sent email to borrower (three notes for this loan) |

| 8 | 4 | Borrower located (skip trace) |

| 8 | 5 | Borrower provided Bankruptcy counsel information |

| 9 | 6 | Borrower filed for Chapter 7 Bankruptcy |

| 9 | 6 | Collections Agency attempted to contact borrower |

| 12 | 8 | Drafting lawsuit |

| 19 | 16 | PAYMENT Failed (previously: Borrower provided Bankruptcy counsel information) |

So now after my big Late Note hit, I'm making some changes. First, Grace Period Notes seem to sell. I think I need to discount them slightly more than I have been. I'll be discounting them to 75% of value instead of 80%. Late Notes don't seem to sell at all (especially 31-120 Days Late). I'm also adjusting my Risk Factor for Note Grade. I used to just convert the letter to a number and the trailing number to the fraction (ie A1 = 1.1, F4 = 6.4). Now I will be squaring that (ie A1 = 1.1^2 = 1.21, F4 = 6.4^2 = 40.96). This should cause my tool to more steeply discount G Grade Notes, as they will be rated 36% more risky instead of 17% more risky. This may also weight my portfolio more towards E Grade Notes. Given the lower return and about equal risk to F Grade Notes, I'm not sure how I feel about that (not to mention my propensity to have Late E Notes).

Also, of note may be the states my Late Notes are from: SC, AZ (2 Notes), NY, VA (3 Notes, same loan), CA, OH (2 Notes), OR, MN. I was already weighting the risk of Notes based on state, thanks to

Nickel Steamroller. Currently I weight riskier than average the following states (riskiest to less risky): CA, FL, NE, IN, MS, TN, IA, ID, MT, UT. I also weight the following states less risky than average (least risky first): WY, ME, OK, LA, CT, KY, NC, WV, KS, AL. I am adding "riskier than average) to my Late Notes' states (although I already had CA as the riskiest, I considered the others as average risk). Since SC and OH have two Late Notes each, I made them as risky as CA and FL. The other states I put their risk about equivalent to TN or IA.

And yes, I have three Notes from the same Loan and the Loan went into Default. I have identified some holes in my detection of Notes from Loans I already own. This is the risk I was trying to avoid. I think I've worked out a way to avoid the hole that got me three notes from the same loan and I think I discount Notes which I have multiple from the same loan.

If I assume that all my Late Notes are worthless, I think I'm basically back to my original investment, so 0% return. So now that I've learned a lot of lessons, I'm starting from the beginning again, and hopefully will come back with a vengeance!