I've now fully invested all the money I've transferred in. I did it slowly, so as to not affect prices too much. I noticed that I did raise the low end for the notes I was investing in.

For a while there, if you looked at 15.5% and higher notes (again Never Late and All Current only) and then sorted by Markup/Discount (sorted low to high) of the top 60 I would own about 80% of them. After three days of only buying notes to replace sold notes and now I only own three of the top 60 discounted notes (15.5% and higher Never Late and All Current).

The notes that I currently hold I've held about 7.3 days average. Given that I bought the bulk of them in the last two weeks due to my increased investment, that makes sense. I've paid an average of $24.63, or in other words I generally buy $25 fractions early in their lifetime. This gives me the most interest for my investment (at the end payments are mostly principal, at the beginning they are mostly interest).

Right now I've got 2.4% more in my account than I put in. Since the bulk of that money was put in in the last two weeks, that would be more than a 50% return per year, if I can keep it up.

I've sold around half as many notes as I currently hold. I've held them for an average of 11.7 days before I sell them. The median Annualized Return on notes I've sold is 59.1%.

Looking over the notes I've sold, about 25% of them have been less than 16% Annualized Return, and most of those have been between -14% to -99%. Some of these have been typos. Some have been an error in my sell calculation (I think). However, given that the other 75% get 17.5% or higher Annualized Return and over 40% of my sales have been at over 100% Annualized Return, I'm still doing pretty well even considering the little glitches and mistakes.

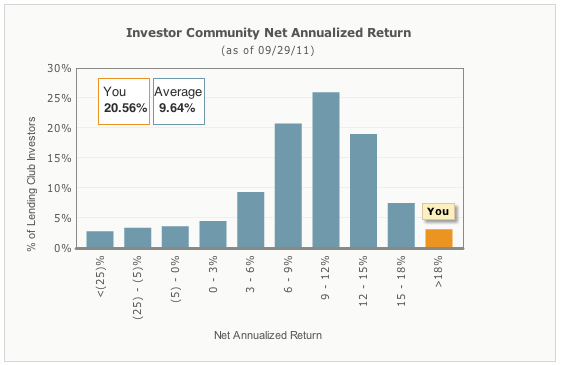

You'll note on the image here that they state that 100 Notes can be purchased with a minimum investment of $2,500. Of course, if you are using the secondary market (Foliofn) you can get 100 Notes for less than that. However, the less you spend on the 100 Notes, the less your return will be. Remember that early in the life of a Note, you get more interest per payment. The smaller the note (the more payments have been made on it), the less interest you'll get in the payments, and hence a lower return also.

Even if you have a lot of Notes, they may still be from the same loan (my tool filters out Notes from loans I already hold).

It looks like most of the 9%+ return crowd go for higher notes. I can understand, as without some tool to manage your notes, it can be a pain to handle a bunch of notes. If you double or triple the size notes you hold, you cut in half or third the number of notes you have to deal with.

Still beginners luck. Still no defaults. Still playing the game. Until next time …

Marc, Very impressive. So, I take it from this post that your strategy is just to hold notes for less than a month before selling them? It is certainly an interesting (and different way) to invest in Lending Club. I look forward to future updates.

ReplyDeleteWould say your approach gets progressively more difficult the more you invest? If you has 20K to invest you would find that unmanageable?

ReplyDeletemphill,

ReplyDeleteIf I had not developed my "assistant" tool, it would become unmanageable. Right now I can handle between 100 and 200 notes with just 10 minutes a day, 5 days a week, so about an hour a week. If it scales linearly (which it doesn't, most of my time is waiting for pages to load), then it will take about 8 hours a week (or a little over an hour a day) to handle 800+ notes.

As I increase the number of notes I have, I am tweaking my "assistant" tool to try to keep it less than 10 minutes a day to maintain this. I'm planning on adding a "time spent" metric to make sure I can keep the time element small.

Peter,

ReplyDeleteMy strategy has ended up being hold a note for less than a month. My intended strategy was to ensure 16%+ return. My philosophy has been if someone wants to buy it from me at a price that gives me 16%+ return, I'd sell it for a guaranteed return.

That has happened to be less than a month, generally. One of the tweaks I am considering making is to increase my minimum return from sale to see if I can find a sweet-spot for time held vs return. If I can hold a note longer, then it will be less time spent buying new notes (most time consuming task so far).

The nice thing about selling a note in less than a month, is that I have not had a default yet. Most of the notes I hold are in their first few months (not as likely to default) and they usually sell before they would even have a chance to default on me.

Again, this has been an accidental byproduct of my 16%+ philosophy. And this is only around 3 months worth of data. I'll keep posting as to how things are going, and we'll see if I can keep it up, and how well this scales.

Marc, Congrats on the press you received today. No doubt you already saw this, but wanted to make sure you did by posting here:

ReplyDeletehttp://www.spokesman.com/blogs/officehours/2011/oct/04/if-youve-become-interested-trying-peer-lending-heres-tip-successful-blogger/

Peter,

ReplyDeleteThanks for the heads up.